Fill Out Your Delaware 1100X Form

Fill Out Your Delaware 1100X Form

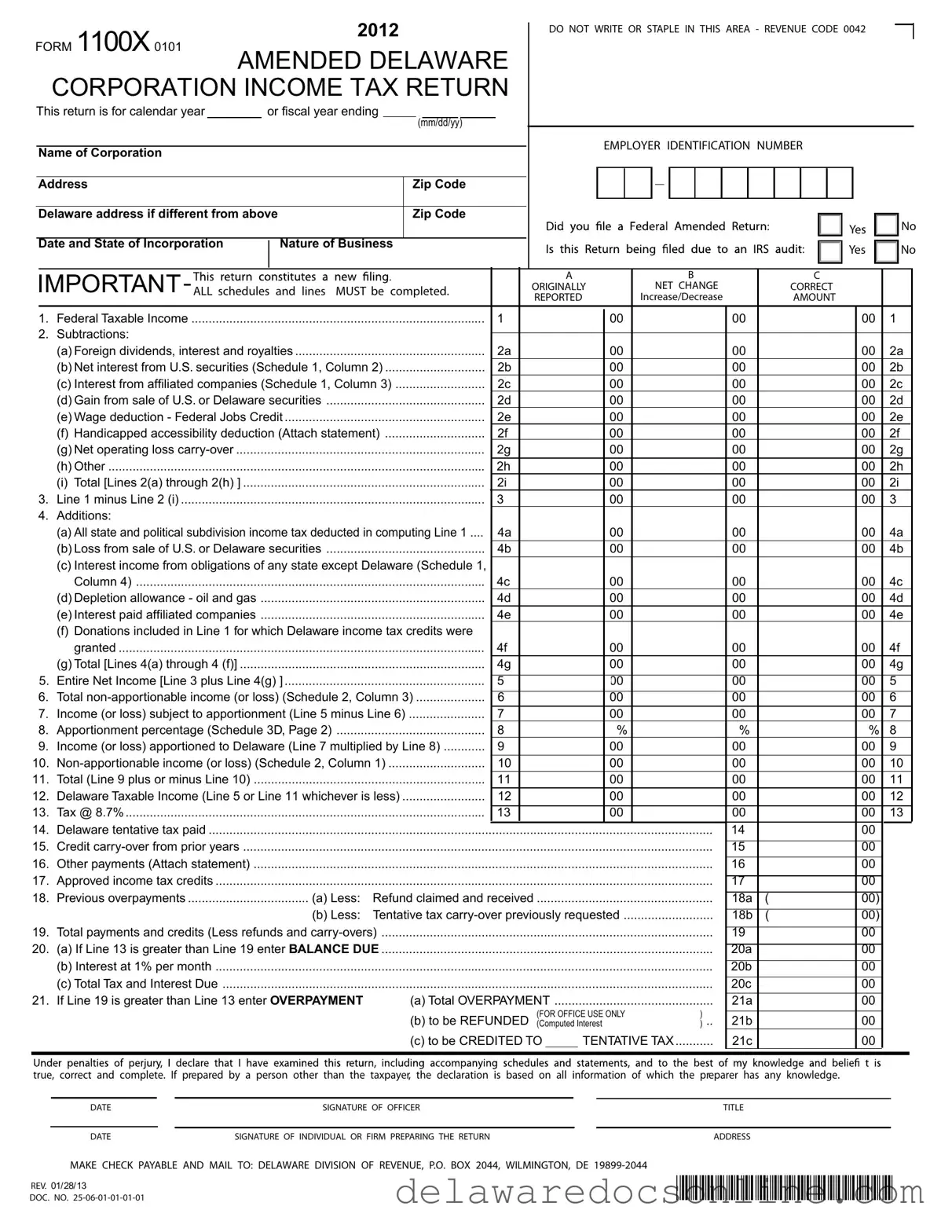

FORM 1100X 0101 |

2012 |

|

DO NOT WRITE OR STAPLE IN THIS AREA - REVENUE CODE 0042 |

|

AMENDED DELAWARE |

|

|||

|

|

|||

CORPORATION INCOME TAX RETURN |

|

|||

This return is for calendar year |

or fiscal year ending |

/ |

/ |

|

|

|

(mm/dd/yy) |

|

|

Name of Corporation |

|

|

EMPLOYER IDENTIFICATION NUMBER |

|

|

|

|

|

|

Address |

|

Zip Code |

|

|

Delaware address if different from above |

Zip Code |

|

||

|

|

|

Yes |

No |

|

|

|

|

|

Date and State of Incorporation |

Nature of Business |

|

Yes |

No |

|

|

|

||

|

|

A |

|

|

|

|

B |

|

|

C |

|

|

|

||||||||||

|

ORIGINALLY |

|

|

NET CHANGE |

|

|

CORRECT |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

REPORTED |

|

|

|

|

INCREASE/DECREASE |

|

|

AMOUNT |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

Federal Taxable Income |

|

|

1 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

1 |

|

|

|||

2. |

Subtractions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

(a) Foreign dividends, interest and royalties |

|

|

2a |

|

|

00 |

|

|

00 |

|

|

00 |

|

2a |

|

|

|||||

|

|

(b) Net interest from U.S. securities (Schedule 1, Column 2) |

2b |

|

|

00 |

|

|

00 |

|

|

00 |

|

2b |

|

|

|||||||

|

|

(c) Interest from affiliated companies (Schedule 1, Column 3) |

2c |

|

|

00 |

|

|

00 |

|

|

00 |

|

2c |

|

|

|||||||

|

|

(d) Gain from sale of U.S. or Delaware securities |

|

2d |

|

|

00 |

|

|

00 |

|

|

00 |

|

2d |

|

|

||||||

|

|

(e) Wage deduction - Federal Jobs Credit |

|

|

2e |

|

|

00 |

|

|

00 |

|

|

00 |

|

2e |

|

|

|||||

|

|

(f) Handicapped accessibility deduction (Attach statement) |

2f |

|

|

00 |

|

|

00 |

|

|

00 |

|

2f |

|

|

|||||||

|

|

(g) Net operating loss |

|

|

2g |

|

|

00 |

|

|

00 |

|

|

00 |

|

2g |

|

|

|||||

|

|

(h) Other |

|

|

2h |

|

|

00 |

|

|

00 |

|

|

00 |

|

2h |

|

|

|||||

|

|

(i) Total [Lines 2(a) through 2(h) ] |

|

|

2i |

|

|

00 |

|

|

00 |

|

|

00 |

|

2i |

|

|

|||||

3. Line 1 minus Line 2 (i) |

|

|

3 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

3 |

|

|

||||

4. |

Additions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) All state and political subdivision income tax deducted in computing Line 1 .... |

4a |

|

|

00 |

|

|

00 |

|

|

00 |

|

4a |

|

|

|||||||

|

|

(b) Loss from sale of U.S. or Delaware securities |

|

4b |

|

|

00 |

|

|

00 |

|

|

00 |

|

4b |

|

|

||||||

|

|

(c) Interest income from obligations of any state except Delaware (Schedule 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Column 4) |

|

|

4c |

|

|

00 |

|

|

00 |

|

|

00 |

|

4c |

|

|

|||||

|

|

(d) Depletion allowance - oil and gas |

|

|

4d |

|

|

00 |

|

|

00 |

|

|

00 |

|

4d |

|

|

|||||

|

|

(e) Interest paid affiliated companies |

|

|

4e |

|

|

00 |

|

|

00 |

|

|

00 |

|

4e |

|

|

|||||

|

|

(f) Donations included in Line 1 for which Delaware income tax credits were |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

granted |

|

|

4f |

|

|

00 |

|

|

00 |

|

|

00 |

|

4f |

|

|

|||||

|

|

(g) Total [Lines 4(a) through 4 (f)] |

|

|

4g |

|

|

00 |

|

|

00 |

|

|

00 |

|

4g |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5. |

Entire Net Income [Line 3 plus Line 4(g) ] |

|

|

5 |

|

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

5 |

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

6. Total |

6 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

6 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

7. Income (or loss) subject to apportionment (Line 5 minus Line 6) |

7 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

7 |

|

|

||||||

8. Apportionment percentage (Schedule 3D, Page 2) |

|

8 |

|

|

|

|

|

% |

|

|

% |

|

|

% |

|

8 |

|

|

|||||

9. Income (or loss) apportioned to Delaware (Line 7 multiplied by Line 8) |

9 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

9 |

|

|

||||||

10. |

10 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

10 |

|

|

||||||

11. |

Total (Line 9 plus or minus Line 10) |

|

|

11 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

11 |

|

|

|||

12. |

Delaware Taxable Income (Line 5 or Line 11 whichever is less) |

12 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

12 |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

13. |

Tax @ 8.7% |

|

|

13 |

|

|

|

|

|

00 |

|

|

00 |

|

|

00 |

|

13 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14. |

Delaware tentative tax paid |

|

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

00 |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15. |

Credit |

|

|

|

|

|

|

|

|

|

|

|

|

15 |

|

|

00 |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16. |

Other payments (Attach statement) |

|

|

|

|

|

|

|

|

|

|

|

|

16 |

|

|

00 |

|

|

|

|

||

17. |

Approved income tax credits |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

17 |

|

|

00 |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

18. |

Previous overpayments |

(a) Less: |

Refund claimed and received |

|

|

|

|

|

18a |

( |

|

00) |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

(b) Less: |

Tentative tax |

|

18b |

( |

|

00) |

|

|

|

|

||||||||||

19. |

Total payments and credits (Less refunds and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

19 |

|

|

00 |

|

|

|

|

|||||||

20. |

(a) If Line 13 is greater than Line 19 enter BALANCE DUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

20a |

|

|

00 |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(b) Interest at 1% per month |

|

|

|

|

|

|

|

|

|

|

|

|

20b |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(c) Total Tax and Interest Due |

|

|

|

|

|

|

|

|

|

|

|

|

20c |

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

21. |

If Line 19 is greater than Line 13 enter OVERPAYMENT |

(a) Total OVERPAYMENT |

|

|

|

|

|

21a |

|

|

00 |

|

|

|

|

||||||||

|

|

|

|

|

|

|

(FOR OFFICE USE ONLY |

) |

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

(b) to be REFUNDED |

21b |

|

|

00 |

|

|

|

|

|||||||||||

|

|

|

|

....................................................(Computed Interest |

|

|

) |

|

|

|

|

|

|

|

|||||||||

|

|

|

|

(c) to be CREDITED TO |

TENTATIVE TAX |

21c |

|

|

00 |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

true, correct and complete. If prepared by a person other than the taxpayer, the declaration is based on all information of which the preparer has any knowledge.

DATE |

|

SIGNATURE OF OFFICER |

|

TITLE |

|

|

|

|

|

DATE |

|

SIGNATURE OF INDIVIDUAL OR FIRM PREPARING THE RETURN |

|

ADDRESS |

MAKE CHECK PAYABLE AND MAIL TO: DELAWARE DIVISION OF REVENUE, P.O. BOX 2044, WILMINGTON, DE

REV. 01/28/13 |

*DF12212019999* |

|

|

DOC. NO. |

|

SCHEDULE 1 - INTEREST INCOME

|

|

Description of |

|

Column 1 |

|

Column 2 |

|

|

|

Column 3 |

|

|

|

Column 4 |

|

|

|

|

Column 5 |

|

|||||||||||

|

|

Interest |

|

Foreign Interest |

|

Interest Received |

Interest Received From |

|

|

Interest Received |

|

|

|

|

Other Interest |

|

|||||||||||||||

|

|

|

|

|

|

|

From U.S. Securities |

|

Affiliated Companies |

|

From State Obligations |

|

Income |

|

|||||||||||||||||

1 |

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

00 |

1 |

||

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

2 |

|

|

|

|

00 |

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

00 |

2 |

|||

3 |

|

|

|

|

00 |

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

00 |

3 |

|||

4 |

|

|

|

|

00 |

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

00 |

4 |

|||

5 |

|

|

|

|

00 |

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

00 |

5 |

|||

6 |

TOTALS |

|

|

00 |

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

|

|

|

00 |

6 |

||||

|

|

SCHEDULE 2 - |

|

|

|

|

|

||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Column 1 |

|

|

Column 2 |

|

|

|

|

Column 3 |

|

|||||||||

|

|

|

|

Description |

|

|

|

|

|

|

Within Delaware |

|

|

Without Delaware |

Total |

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

1 |

Rents and royalties from tangible property |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

1 |

||||||||||

|

2 |

Royalties from patents and copyrights |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

2 |

||||||||||

|

3 |

Gains or (losses) from sale of real property |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

3 |

||||||||||

|

4 |

Gains or (losses) from sale of depreciable tangible property |

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

4 |

||||||||||||

|

5 |

Interest income from Schedule 1, Columns 4 and 5 |

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

5 |

||||||||||||

6 |

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

6 |

|||||||

|

7 |

Less: Applicable expenses (Attach statement) |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

7 |

||||||||||

8 |

|

Total |

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

00 |

|

00 |

8 |

||||||||||

|

|

SCHEDULE 3 - APPORTIONMENT PERCENTAGE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

Schedule |

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Description |

|

|

|

Within Delaware |

|

|

Within and Without Delaware |

|

|||||||||||||||||||

|

|

|

|

|

Beginning of Year |

End of Year |

|

|

Beginning of Year |

|

End of Year |

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

1 |

Real and tangible property owned |

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

00 |

|

||||||

|

|

Real and tangible property rented |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

2 |

(Eight times annual rental paid) |

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

00 |

2 |

|||||||

3 |

|

Total |

|

|

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

00 |

3 |

||||

|

|

Less: Value at original cost of real and tangible property |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

4 |

the income from which is separately allocated |

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

00 |

|

|||||||

5 |

|

Total |

|

|

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

|

|

00 |

|

|

|

00 |

5 |

||||

6 |

|

Average value |

............................................................. |

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

|

00 |

6 |

|||

|

|

|

|

Schedule |

|

|

|

|

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Description |

|

|

|

|

|

|

Within Delaware |

|

|

|

|

|

Within and |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without Delaware |

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

|

||||||||||

|

Wages, salaries, and other compensation of all employees |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

1 |

||||||||||

|

Less: Wages, salaries, and other compensation of general executive officers |

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

2 |

|||||||||||||||

3 |

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

3 |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

Schedule |

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

Description |

|

|

|

|

|

|

Within Delaware |

|

|

|

|

|

Within and |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Without Delaware |

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

Gross receipts from sales of tangible personal property |

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

00 |

1 |

|||||||||

|

Gross income from other sources (Attach statement) |

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

00 |

2 |

||||||||||||

3 |

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|

|

|

00 |

3 |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

Schedule |

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

Average value of real and tangible property within Delaware |

|

|

|

|

|

|

|

|

|

00 |

|

= |

|

|

% |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

||||||||||||||

|

|

Average value of real and tangible property within and without Delaware |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

Wages, salaries and other compensation paid to employees within Delaware |

|

. |

|

|

|

|

00 |

|

= |

|

|

% |

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

|||||||||||||||||

|

|

Wages, salaries and other compensation paid to employees within and without Delaware |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

Gross receipts and gross income from within Delaware |

|

|

|

|

|

|

|

|

|

00 |

|

= |

|

|

% |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|

|

|

||||||||||||||

|

|

Gross receipts and gross income from within and without Delaware |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

Apportionment percentage |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

*DF12212029999*

REV. 01/13

Filling out the Delaware 1100X form is essential for amending your corporation's income tax return. This process requires careful attention to detail to ensure accuracy. Follow these steps to complete the form correctly.

When filing the Delaware 1100X form, which is an amended corporate income tax return, it’s essential to be aware of other related forms and documents that may be necessary. These forms help ensure that your tax filings are complete and accurate. Below is a list of five commonly used forms that often accompany the Delaware 1100X.

Understanding these accompanying forms is vital for a smooth filing process. Ensuring that all necessary documents are completed accurately can help avoid delays and potential penalties. Take the time to review each form carefully and consult with a tax professional if needed.

Ensure that all sections of the Delaware 1100X form are completed. Missing information can lead to processing delays or errors in tax calculations.

Double-check the Employer Identification Number and the corporation's name. Accurate identification is crucial for proper tax filing.

Review the subtractions and additions carefully. These adjustments can significantly affect the taxable income reported on the form.

Calculate the apportionment percentage using the provided schedules. This percentage determines how much income is subject to Delaware tax.

Submit the completed form and any required payments to the Delaware Division of Revenue promptly to avoid penalties or interest on unpaid taxes.

Delaware Ap1 - A thorough review of the report before submission can help prevent issues or discrepancies later.

To ensure the accuracy of the information provided, many employers rely on the Employment Verification Form, which allows them to confirm the employment status of current or former employees. This document not only captures crucial details such as the employee's position and dates of employment but also plays a vital role in processes like background checks, loan applications, and housing requests. For those seeking a template for this form, TopTemplates.info offers a comprehensive resource.

Delaware Registry - Provide a clear explanation if you have any substantiated cases.

| Fact Name | Details |

|---|---|

| Form Purpose | The Delaware 1100X form is used to file an amended corporation income tax return. |

| Governing Law | This form is governed by Delaware state tax laws, specifically Title 30 of the Delaware Code. |

| Filing Period | Corporations can use this form for calendar or fiscal years ending on a specified date. |

| Employer Identification Number | Corporations must provide their Employer Identification Number (EIN) on the form. |

| Important Instructions | All schedules and lines on the form must be completed for the return to be valid. |

| Tax Rate | The tax rate applied on the Delaware taxable income is 8.7%. |

| Payment Instructions | Payments should be made out to the Delaware Division of Revenue and mailed to the specified address. |

| Overpayment and Refunds | If the total payments exceed the tax owed, the corporation may claim an overpayment for refund or credit. |