Fill Out Your Delaware 200 Es Form

Fill Out Your Delaware 200 Es Form

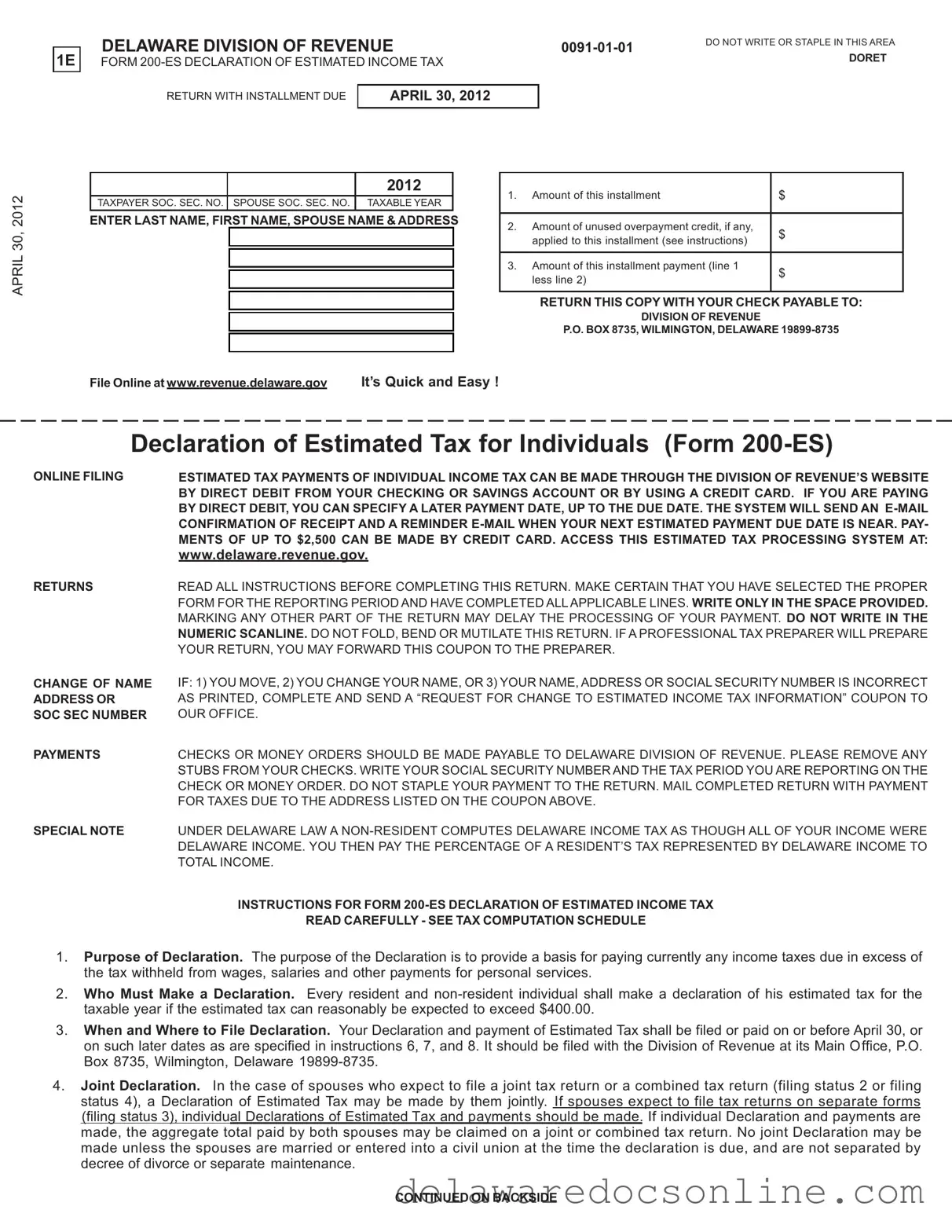

1E

DELAWARE DIVISION OF REVENUE |

DO NOT WRITE OR STAPLE IN THIS AREA |

|||

DORET |

||||

FORM |

|

|||

|

|

|||

|

|

|

|

|

RETURN WITH INSTALLMENT DUE |

APRIL 30, 2012 |

|

|

|

|

|

|

|

|

APRIL 30, 2012

2012

TAXPAYER SOC. SEC. NO. SPOUSE SOC. SEC. NO. TAXABLE YEAR

ENTER LAST NAME, FIRST NAME, SPOUSE NAME & ADDRESS

1. |

Amount of this installment |

$ |

|

|

|||

|

|

|

|

|

|

|

|

2. |

Amount of unused overpayment credit, if any, |

$ |

|

|

|||

|

applied to this installment (see instructions) |

|

|

|

|

|

|

|

|

|

|

3. |

Amount of this installment payment (line 1 |

$ |

|

|

|||

|

less line 2) |

|

|

|

|

|

|

|

|

|

|

RETURN THIS COPY WITH YOUR CHECK PAYABLE TO:

DIVISION OF REVENUE

P.O. BOX 8735, WILMINGTON, DELAWARE

File Online at www.revenue.delaware.gov |

It’s Quick and Easy ! |

Declaration of Estimated Tax for Individuals (Form

ONLINE FILING |

ESTIMATED TAX PAYMENTS OF INDIVIDUAL INCOME TAX CAN BE MADE THROUGH THE DIVISION OF REVENUE’S WEBSITE |

|

BY DIRECT DEBIT FROM YOUR CHECKING OR SAVINGS ACCOUNT OR BY USING A CREDIT CARD. IF YOU ARE PAYING |

|

BY DIRECT DEBIT, YOU CAN SPECIFY A LATER PAYMENT DATE, UP TO THE DUE DATE. THE SYSTEM WILL SEND AN |

|

CONFIRMATION OF RECEIPT AND A REMINDER |

|

MENTS OF UP TO $2,500 CAN BE MADE BY CREDIT CARD. ACCESS THIS ESTIMATED TAX PROCESSING SYSTEM AT: |

RETURNS

CHANGE OF NAME ADDRESS OR SOC SEC NUMBER

PAYMENTS

SPECIAL NOTE

www.delaware.revenue.gov.

READ ALL INSTRUCTIONS BEFORE COMPLETING THIS RETURN. MAKE CERTAIN THAT YOU HAVE SELECTED THE PROPER FORM FOR THE REPORTING PERIOD AND HAVE COMPLETED ALL APPLICABLE LINES. WRITE ONLY IN THE SPACE PROVIDED. MARKING ANY OTHER PART OF THE RETURN MAY DELAY THE PROCESSING OF YOUR PAYMENT. DO NOT WRITE IN THE NUMERIC SCANLINE. DO NOT FOLD, BEND OR MUTILATE THIS RETURN. IF A PROFESSIONAL TAX PREPARER WILL PREPARE YOUR RETURN, YOU MAY FORWARD THIS COUPON TO THE PREPARER.

IF: 1) YOU MOVE, 2) YOU CHANGE YOUR NAME, OR 3) YOUR NAME, ADDRESS OR SOCIAL SECURITY NUMBER IS INCORRECT AS PRINTED, COMPLETE AND SEND A “REQUEST FOR CHANGE TO ESTIMATED INCOME TAX INFORMATION” COUPON TO OUR OFFICE.

CHECKS OR MONEY ORDERS SHOULD BE MADE PAYABLE TO DELAWARE DIVISION OF REVENUE. PLEASE REMOVE ANY STUBS FROM YOUR CHECKS. WRITE YOUR SOCIAL SECURITY NUMBER AND THE TAX PERIOD YOU ARE REPORTING ON THE CHECK OR MONEY ORDER. DO NOT STAPLE YOUR PAYMENT TO THE RETURN. MAIL COMPLETED RETURN WITH PAYMENT FOR TAXES DUE TO THE ADDRESS LISTED ON THE COUPON ABOVE.

UNDER DELAWARE LAW A

INSTRUCTIONS FOR FORM

READ CAREFULLY - SEE TAX COMPUTATION SCHEDULE

1.Purpose of Declaration. The purpose of the Declaration is to provide a basis for paying currently any income taxes due in excess of the tax withheld from wages, salaries and other payments for personal services.

2.Who Must Make a Declaration. Every resident and

3.When and Where to File Declaration. Your Declaration and payment of Estimated Tax shall be filed or paid on or before April 30, or on such later dates as are specified in instructions 6, 7, and 8. It should be filed with the Division of Revenue at its Main Office, P.O. Box 8735, Wilmington, Delaware

4.Joint Declaration. In the case of spouses who expect to file a joint tax return or a combined tax return (filing status 2 or filing status 4), a Declaration of Estimated Tax may be made by them jointly. If spouses expect to file tax returns on separate forms (filing status 3), individual Declarations of Estimated Tax and payments should be made. If individual Declaration and payments are made, the aggregate total paid by both spouses may be claimed on a joint or combined tax return. No joint Declaration may be made unless the spouses are married or entered into a civil union at the time the declaration is due, and are not separated by decree of divorce or separate maintenance.

CONTINUED ON BACKSIDE

5.Farmers and Fishermen. If at least

6.Fiscal Year. If you file your income tax return on a fiscal year basis, your dates for filing the Declaration and payment of the Estimated Tax will be the 30th day of the fourth month and the 15th day of the sixth and ninth months of your current fiscal year and the 15th day of the 1st month of the next fiscal year.

7.Changes in Income, Exemption(s) or Deduction(s). (a) Even though your situation on April 30 is such that you are not required to file a Declaration at that time, your expected income, exemption(s) or deduction(s) may change so that you will be required to file a Declaration later. In such case the time for filing is as follows: June 15, if the change occurs after April 1 and before June 2; September 17 if the change occurs after June 1 and before September 2; January 15 of the following year if the change occurs after September 1. The Estimated Tax may be paid in full at the time of filing the Declaration or in equal installments on the remaining payment dates. (b) After you have filed a Declaration, if changes in income, exemptions, or deductions cause a substantial increase or decrease in Estimated Tax, you should adjust Line 8 of the Tax Computation Schedule (worksheet) and enter the adjusted amount on Line 1 of each remaining Form 200- ES and forward on the required due dates. (It will no longer be required to file a Form

8.Payment of Estimated Tax. Your Estimated Tax may be paid in full with the Declaration, or in equal installments on or before April 30, June 15, September 17, and January 15 of the following year. The first installment must accompany the Declaration. The last installment must be mailed no later than January 15 of the following year.

9.Method of Payments. Form

Method 1. Full Credit. In using this method, you must apply the full amount of credit against first and succeeding installments until fully used. Reflect the full amount of overpayment credit from preceding year on Line 9 of the Tax Computation Schedule worksheet and on Line 2 of Form

Method 2. Quarterly Installment Credits. Reflect the full amount of overpayment credit from preceding year on Line 9 of the Tax Computation Schedule, divide this amount by the number of installments required to be made, and enter the amount on line 2 of each Form

10.Penalty for Failure to Pay Estimated Income Tax. A penalty of 11/2% per month or fraction thereof may be imposed on the underpay- ment of any installment of estimated tax except in certain situations. The penalty does not apply if each installment is paid on time and (a) is at least 90 percent (662/3% for farmers and fishermen) of the amount due on the income tax return for the taxable year, or (b) 100% of the tax shown on the prior year's return, (110% if the federal Adjusted Gross Income for the previous tax year is in excess of $150,000 ($75,000 if married or entered into a civil union filing separate)). Payment of estimated tax is not required if there was no tax liability for the preceding year, provided such year was a

11.Waiver of Penalty. The underpayment penalty may be waived if the underpayment is due to casualty, disaster or other unusual circum- stances. Note, however, that these grounds will not be apparent during processing of a tax return and must be raised by the taxpayer in a request for abatement of any penalty assessed.

|

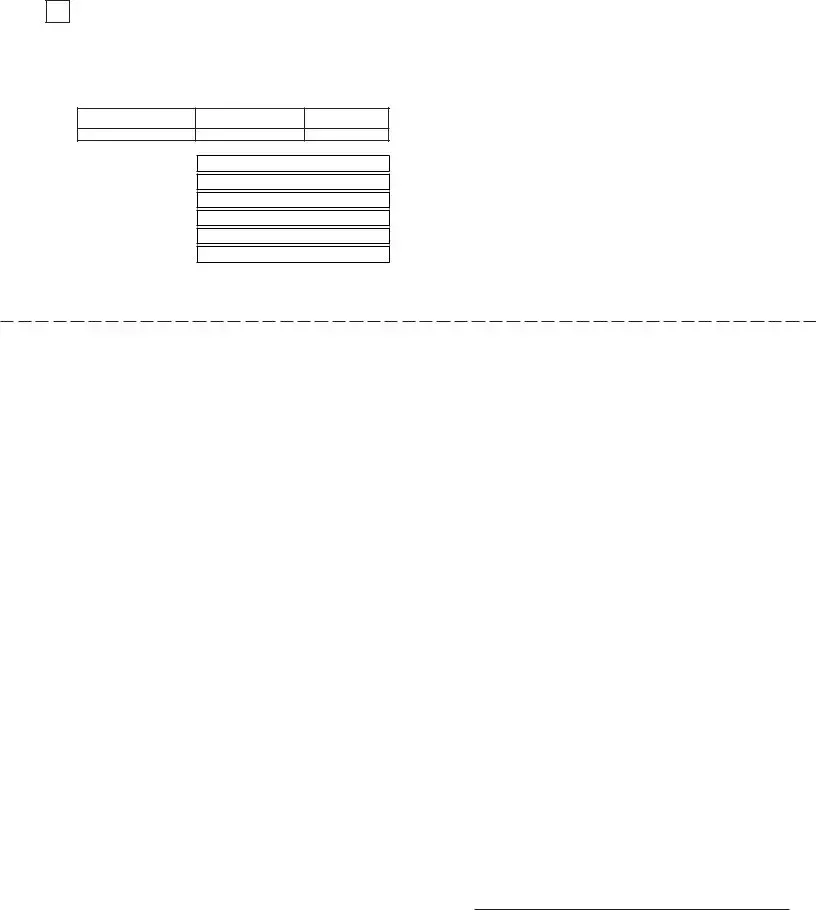

TAX COMPUTATION SCHEDULE (Keep For Your Records) |

|

1. |

Enter Amount of total gross income expected for the year |

$ |

2. |

Less: total of: (a) Pension Exclusions - per person ($2000 under 60 years of age/$12,500 if 60 or over); |

|

(b) Over 60 Exclusions; and, (c) Interest from U.S. Obligations |

$ |

3.(A) If deductions will be itemized, enter estimated itemized deductions total

|

|

If not itemizing, use Standard Deduction ($3250 single, divorced or widow(er), head of household) |

|

|

|

|

|

|

||||||||||

|

|

($6500 if married or entered into a civil union filing jointly), or ($3250 if married or entered into |

|

$ |

|

|

|

|

||||||||||

|

|

a civil union filing separately) |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

(B) Additional Standard Deduction Allowance(s) of $2500 for taxpayer &/or spouse |

|

|

|

|

|

|

|

|||||||||

|

|

if 65 years old or over or blind and filing Standard Deductions |

|

|

|

|

$ |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|||||||||

4. |

Total of lines 2 and 3 |

.......................................................................................................................................... |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

||

5. |

....................................................................................................Estimated Taxable Income (line 1 less line 4) |

|

|

|

|

|

|

$ |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||||||||

6. |

Estimated Tax Liability (use Tax Computation Table below to compute this entry) |

........................................... |

|

$ |

|

|

|

|

||||||||||

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Over |

But not over |

Tax is |

|

|

In excess |

|

|

Over |

But not |

Tax is |

|

|

|

In excess |

|||

|

|

2,000.00 |

|

0 |

|

|

of |

|

|

|

over |

|

|

|

|

|

of |

|

$2,000.00 |

5,000.00 |

$ 0.00 |

|

2.20% |

(.0220) |

$ 2.000.00 |

|

|

20,000.00 |

25,000.00 |

741.00 |

+ |

5.20% |

(.0520) |

$20,000.00 |

|||

|

5,000.00 |

10,000.00 |

66.00 |

+ |

3.90% |

(.0390) |

5,000.00 |

|

|

25,000.00 |

60,000.00 |

1,001.00 |

+ |

5.55% |

(.0555) |

25,000.00 |

||

10,000.00 |

20,000.00 |

261.00 |

+ |

4.80% |

(.0480) |

10,000.00 |

|

|

60.000.00 |

and over |

2,943.50 |

+ |

6.75% |

(.0675) |

60.000.00 |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7.Personal Credits ($110.00 X total number of Federal Exemptions and exemptions

for being 60 or older) |

$ |

8.Estimate of: (a) income tax to be withheld during year; (b) credit for income

|

tax paid to another state; (c) volunteer firefighters, fire auxiliary & rescue squad credit; |

|

|

(d) childcare credit; (e) other |

$ |

9. Estimated Tax Credit to be carried forward from 2011 return |

$ |

|

10. |

Total Credits (Lines 7, 8 and 9) |

$ |

11. |

Total Estimated Tax Liability (line 6 less line 10) |

$ |

12. |

Quarterly Payment Amount (Divide line 11 by a factor of 4.) |

$ |

Completing the Delaware Form 200-ES requires careful attention to detail. This form is essential for individuals who need to declare their estimated income tax and make timely payments. Following the steps outlined below will ensure that the form is filled out correctly and submitted on time.

The Delaware 200-ES form is essential for individuals who need to declare their estimated income tax. However, it is often accompanied by several other forms and documents that help ensure compliance with tax regulations. Understanding these documents can make the process smoother and more efficient.

Familiarizing yourself with these forms can help ensure that your tax filings are accurate and timely. Proper documentation reduces the risk of penalties and simplifies the overall tax process.

Filling out and using the Delaware 200-ES form requires careful attention to detail. Here are seven key takeaways to ensure compliance and accuracy:

Understanding these key points can help ensure that taxpayers fulfill their obligations effectively and avoid unnecessary penalties.

Power of Attorney Form Delaware - The form references specific sections of the Delaware Code that explain the powers and duties of an Agent.

For those looking to formalize their pet transactions, an informative resource is available that outlines the importance of the Dog Bill of Sale in California. This crucial document facilitates the proper transfer of ownership and ensures clarity throughout the sale process. Check it out here: essential California Dog Bill of Sale information.

Does Delaware Tax Social Security - Check the descriptions carefully on the back of the 1089 to ensure correct form selection.

| Fact Name | Description |

|---|---|

| Purpose | The Delaware 200-ES form is used for declaring estimated income tax for individuals, ensuring timely payment of taxes due beyond what is withheld from wages. |

| Filing Requirement | Both residents and non-residents must file a declaration if their estimated tax exceeds $400 for the taxable year. |

| Due Dates | Estimated tax payments are due on April 30, June 15, September 17, and January 15 of the following year. |

| Joint Filings | Spouses may file a joint declaration if they plan to submit a joint tax return. Separate filings are necessary if they intend to file individually. |

| Payment Methods | Payments can be made online via direct debit or credit card. The system allows for scheduling payments and sends confirmation emails. |

| Penalty for Underpayment | A penalty of 1.5% per month may apply to any underpayment of estimated tax unless certain conditions are met. |

| Governing Law | The Delaware 200-ES form is governed by Delaware state tax laws, specifically regarding income tax obligations for individuals. |