Fill Out Your Delaware 300 Form

Fill Out Your Delaware 300 Form

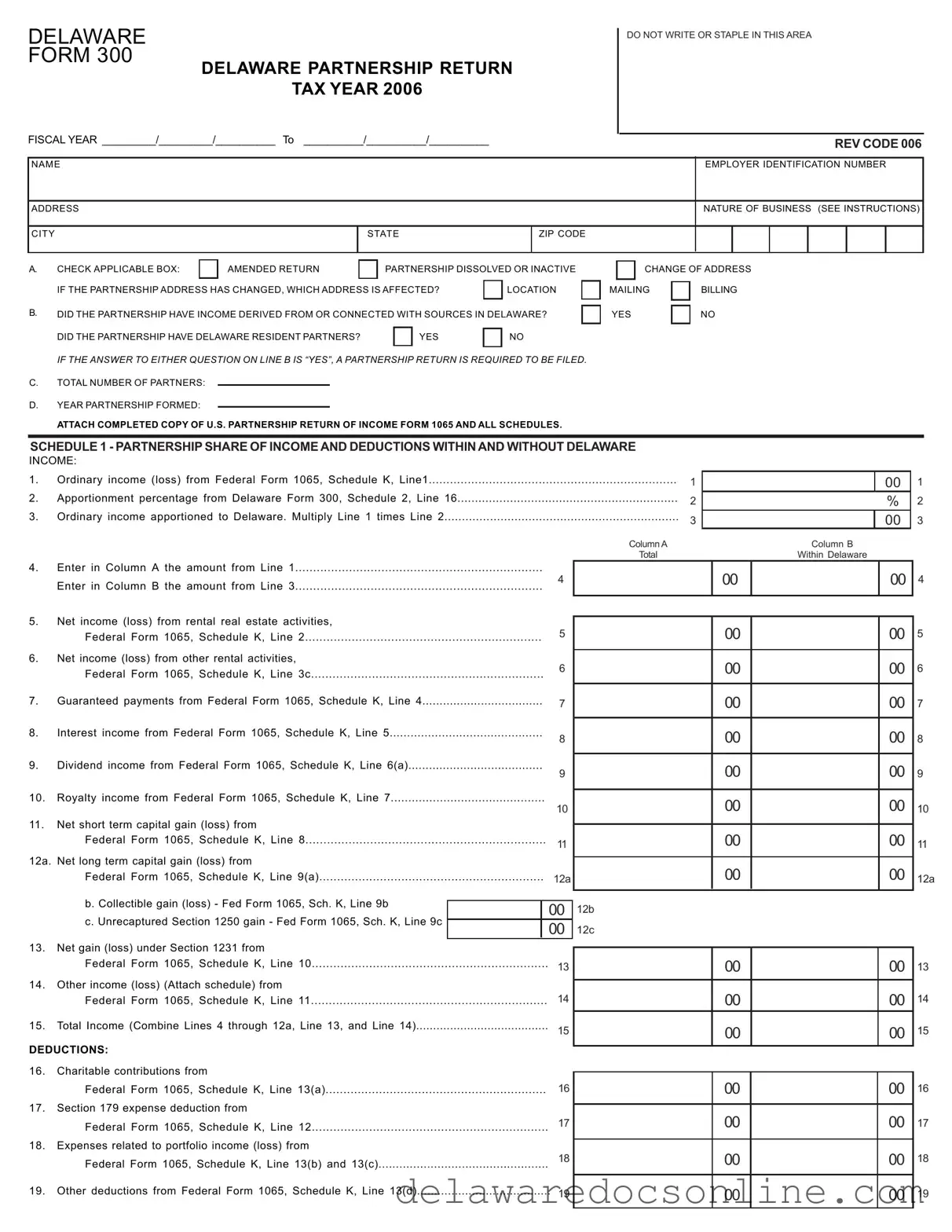

DELAWARE

FORM 300

DELAWARE PARTNERSHIP RETURN

TAX YEAR 2006

DO NOT WRITE OR STAPLE IN THIS AREA

FISCAL YEAR _________/_________/__________ To |

__________/__________/__________ |

|

|

|

|

|

REV CODE 006 |

|||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

NAME |

|

|

|

|

EMPLOYER IDENTIFICATION NUMBER |

|||||

|

|

|

|

|

|

|

|

|

|

|

ADDRESS |

|

|

|

|

NATURE OF BUSINESS (SEE INSTRUCTIONS) |

|||||

|

|

|

|

|

|

|

|

|

|

|

CITY |

|

STATE |

ZIP CODE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

A. CHECK APPLICABLE BOX: |

|

AMENDED RETURN |

|

PARTNERSHIP DISSOLVED OR INACTIVE |

||

IF THE PARTNERSHIP ADDRESS HAS CHANGED, WHICH ADDRESS IS AFFECTED? |

|

LOCATION |

||||

|

|

|

|

|

|

|

B.DID THE PARTNERSHIP HAVE INCOME DERIVED FROM OR CONNECTED WITH SOURCES IN DELAWARE?

DID THE PARTNERSHIP HAVE DELAWARE RESIDENT PARTNERS? |

|

YES |

|

NO |

|

|

|

|

|

IF THE ANSWER TO EITHER QUESTION ON LINE B IS “YES”, A PARTNERSHIP RETURN IS REQUIRED TO BE FILED.

C.TOTAL NUMBER OF PARTNERS:

D.YEAR PARTNERSHIP FORMED:

ATTACH COMPLETED COPY OF U.S. PARTNERSHIP RETURN OF INCOME FORM 1065 AND ALL SCHEDULES.

CHANGE OF ADDRESS

MAILING |

|

BILLING |

|

|

|

YES |

|

NO |

|

||

|

|

|

SCHEDULE 1 - PARTNERSHIP SHARE OF INCOME AND DEDUCTIONS WITHINAND WITHOUT DELAWARE

INCOME: |

|

|

1. |

Ordinary income (loss) from Federal Form 1065, Schedule K, Line1 |

1 |

2. |

Apportionment percentage from Delaware Form 300, Schedule 2, Line 16 |

|

|

|

2 |

3. |

Ordinary income apportioned to Delaware. Multiply Line 1 times Line 2 |

|

|

|

3 |

|

|

Column A |

|

|

Total |

00

%

00

Column B

Within Delaware

1

2

3

4. Enter in Column A the amount from Line 1.....................................................................

Enter in Column B the amount from Line 3.....................................................................

4

00

004

5. Net income (loss) from rental real estate activities, |

|

|

5 |

Federal Form 1065, Schedule K, Line 2 |

|

6. Net income (loss) from other rental activities, |

|

|

6 |

Federal Form 1065, Schedule K, Line 3c |

|

7. Guaranteed payments from Federal Form 1065, Schedule K, Line 4 |

|

|

7 |

8. Interest income from Federal Form 1065, Schedule K, Line 5 |

|

|

8 |

9. Dividend income from Federal Form 1065, Schedule K, Line 6(a) |

|

|

9 |

10. Royalty income from Federal Form 1065, Schedule K, Line 7 |

|

|

10 |

11. Net short term capital gain (loss) from |

|

Federal Form 1065, Schedule K, Line 8 |

|

|

11 |

12a. Net long term capital gain (loss) from |

|

Federal Form 1065, Schedule K, Line 9(a) |

12a |

b. Collectible gain (loss) - Fed Form 1065, Sch. K, Line 9b |

|

|

00 |

c. Unrecaptured Section 1250 gain - Fed Form 1065, Sch. K, Line 9c |

|

|

00 |

13. Net gain (loss) under Section 1231 from |

|

Federal Form 1065, Schedule K, Line 10 |

|

|

13 |

14. Other income (loss) (Attach schedule) from |

|

Federal Form 1065, Schedule K, Line 11 |

14 |

15. Total Income (Combine Lines 4 through 12a, Line 13, and Line 14) |

|

|

15 |

DEDUCTIONS: |

|

16.Charitable contributions from

|

Federal Form 1065, Schedule K, Line 13(a) |

16 |

17. |

Section 179 expense deduction from |

|

|

|

17 |

|

Federal Form 1065, Schedule K, Line 12 |

|

18. |

Expenses related to portfolio income (loss) from |

|

|

|

18 |

|

Federal Form 1065, Schedule K, Line 13(b) and 13(c) |

|

19. |

Other deductions from Federal Form 1065, Schedule K, Line 13(d) |

|

|

|

19 |

12b

12c

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

005

006

007

008

009

0010

0011

0012a

0013

0014

0015

0016

0017

0018

0019

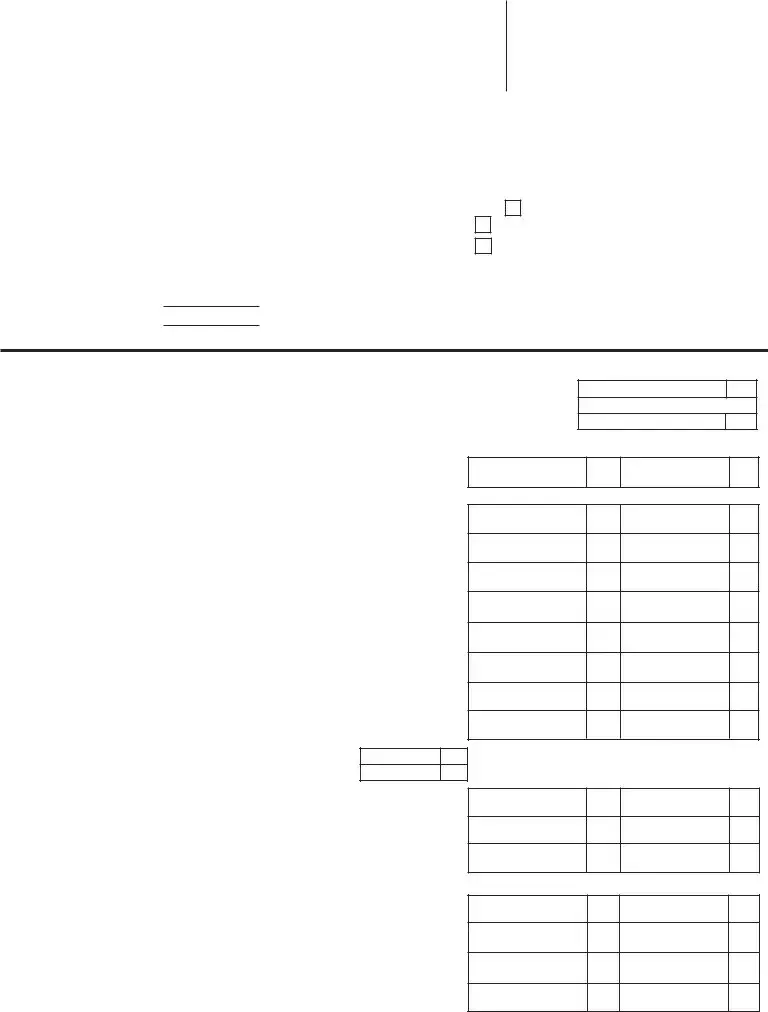

SCHEDULE 2 - APPORTIONMENT PERCENTAGE: COMPLETE ONLY IF PARTNERSHIP HAS INCOME DERIVED FROM OR CONNECTED WITH SOURCES IN DELAWARE AND AT LEAST ONE OTHER STATE AND IF IT HAS ONE OR MORE PARTNERS WHO ARE NOT RESIDENTS IN DELAWARE.

SECTION A - GROSS REAL AND TANGIBLE PERSONAL PROPERTY

COLUMN A |

|

COLUMN B |

|

Delaware Sourced |

|

Total Sourced (All Sources) |

|

Beginning of Year |

End of Year |

Beginning of Year |

End of Year |

1.Total real and tangible property owned..............................................................

2.Real tangible property rented (eight times annual rent paid).................................

3.Total (Combine Lines 1 and 2).........................................................................

4.Less: value at original cost of real and tangible property (see instructions)...........

5.Net Values (Subtract Line 4 from Line 3)..........................................................

6. |

Total (Combine Line 5 Beginning and End of Year Totals) |

6 |

7. |

Average values. (Divide Line 6 by 2) |

7 |

1

2

3

4

5

SECTION B - WAGES, SALARIES,AND OTHER COMPENSATION PAID ORACCRUED TO EMPLOYEES

8. Wages, salaries and other compensation of all employees....................................................

8

SECTION C - GROSS RECEIPTS SUBJECT TO APPORTIONMENT

9.Gross receipts from sales of tangible personal property........................................................

10.Gross income from other sources (see attachment)............................................................

11.Total..............................................................................................................................

9

10

11

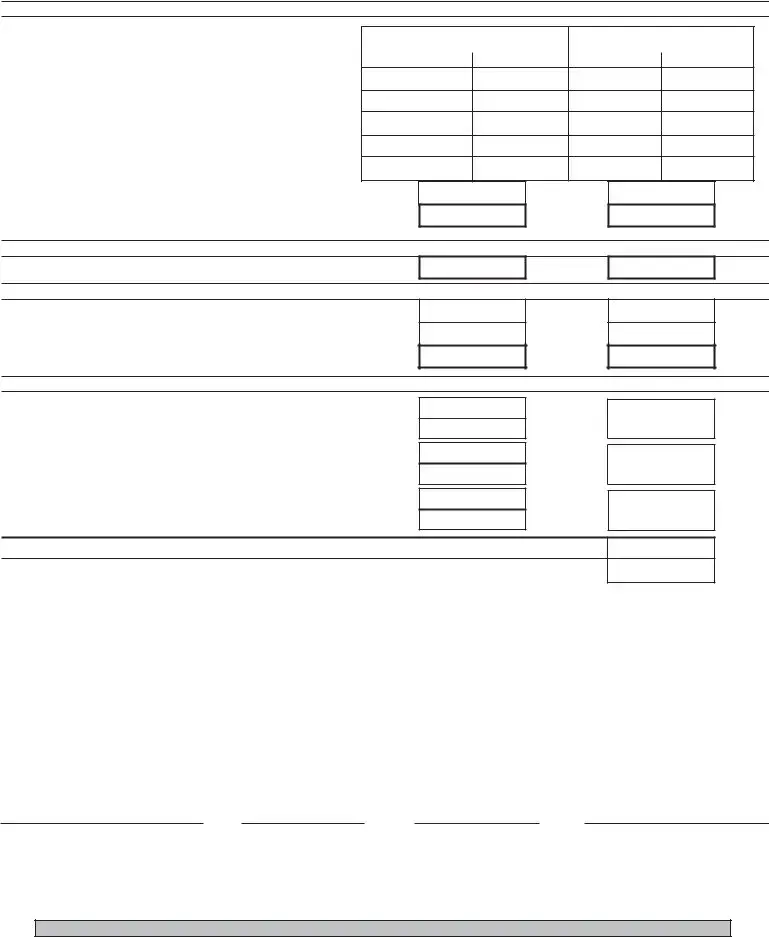

SECTION D - DETERMINATION OF APPORTIONMENT PERCENTAGES

12a. Enter amount from Column A, Line 7..............................................................................

=

12b. Enter amount from Column B, Line 7..............................................................................

13a. Enter amount from Column A, Line 8..............................................................................

=

13b. Enter amount from Column B. Line 8..............................................................................

14a. Enter amount from Column A, Line 11.............................................................................

=

14b. Enter amount from Column B, Line 11.............................................................................

15.Total (Combine Apportionment Percentages on Lines 12, 13 and 14)

16.Apportionment percentage (see specific instructions)............................................................................................................................................................................................................................

%

%

%

%

12a

12b

13a

13b

14a

14b

15

16

UNDER PENALTIES OF PERJURY, I DECLARE THAT I HAVE EXAMINED THIS RETURN, INCLUDING ACCOMPANYING SCHEDULES AND STATEMENTS, AND TO THE BEST OF MY KNOWLEDGE AND BELIEF IT IS TRUE, CORRECT, AND COMPLETE. IF PREPARED BY A PERSON OTHER THAN TAXPAYER, THIS DECLARATION IS BASED ON ALL INFORMATION OF WHICH HE/SHE HAS ANY KNOWLEDGE.

SIGNATURE OF PARTNER |

DATE |

|

TELEPHONE NUMBER |

|

||

|

|

|

|

|

|

|

SIGNATURE OF PREPARER |

DATE |

|

TELEPHONE NUMBER |

|

PRINT NAME OF PREPARER |

|

|

|

|

|

|

|

|

PREPARER ADDRESS (STREET, CITY, STATE & ZIP CODE) |

|

|

|

|

PREPARER EIN/SSN/PTIN |

|

MAIL TO: DIVISION OF REVENUE, P.O. BOX 8703, WILMINGTON, DELAWARE

(Revised 01/22/07)

Completing the Delaware 300 form is an important task for partnerships operating in the state. Once you have filled out the form, it will need to be submitted to the Division of Revenue in Delaware. Follow these steps carefully to ensure that all necessary information is accurately provided.

The Delaware Form 300 is a critical document used by partnerships to report income and deductions for tax purposes. Alongside this form, several other documents are typically required to provide a complete picture of the partnership's financial activities. Below are four commonly associated forms and documents.

These documents collectively ensure that partnerships comply with both federal and state tax regulations. Proper completion and submission of each form are vital to avoid penalties and ensure accurate tax reporting.

When filling out the Delaware 300 form, it is essential to understand several key aspects to ensure compliance and accuracy. Here are nine important takeaways:

By keeping these points in mind, you can navigate the process of filling out the Delaware 300 form more effectively.

Delaware 5403 - The Delaware Division of Revenue processes the information submitted on this form.

Delaware Pardon Application - Be aware of the possibility that your request for a hearing may require approval.

For anyone considering the acquisition of a pet, understanding the importance of a formal agreement is crucial. The process can be simplified by utilizing a comprehensive Dog Bill of Sale document, which serves as a crucial record of the transaction and the dog's ownership transfer. You can find more about this important document in this valuable guide.

Delaware Seller's Permit - Form 373 represents a vital tool for businesses that operate across state lines in Delaware.

| Fact Name | Fact Details |

|---|---|

| Purpose | The Delaware 300 form is used to file the partnership return for tax purposes. |

| Tax Year | This form is specifically for the tax year 2006. |

| Filing Requirement | A partnership return is required if the partnership has income derived from Delaware sources or has Delaware resident partners. |

| Amended Returns | There is a box to check if the return is amended or if the partnership is dissolved or inactive. |

| Partnership Information | Partnership details such as name, address, and employer identification number must be provided. |

| Income Reporting | Partners must report ordinary income, rental income, and other types of income as specified in the form. |

| Deductions | Eligible deductions, including charitable contributions and Section 179 expense deductions, can be reported on the form. |

| Apportionment | The form includes a section for calculating the apportionment percentage for income derived from Delaware and other states. |

| Signature Requirement | The return must be signed by a partner and the preparer, if applicable, along with their contact information. |

| Governing Law | The Delaware 300 form is governed by Delaware state tax laws. |